New Zealand

AIR

IMPORT

- Major terminals (Air New Zealand, Swissport, Menzies) are operating normally nationwide.

EXPORT

- Major terminals (Air New Zealand, Swissport, Menzies) are operating normally nationwide.

LANDSIDE & CUSTOMS

- New Zealand Exports – Due to the conflict in Iran and the resulting increase in fuel costs delivery rates for DAP & DDP shipments will increase for shipments booked and in transit. Should your shipment be affected we will be in contact once costs are known.

- KiwiRail Block Of Line for Auckland over Easter Weekend. No Containers moving between Metroport and Tauranga either way during the 4 day weekend, there will be delays to containers across this route.

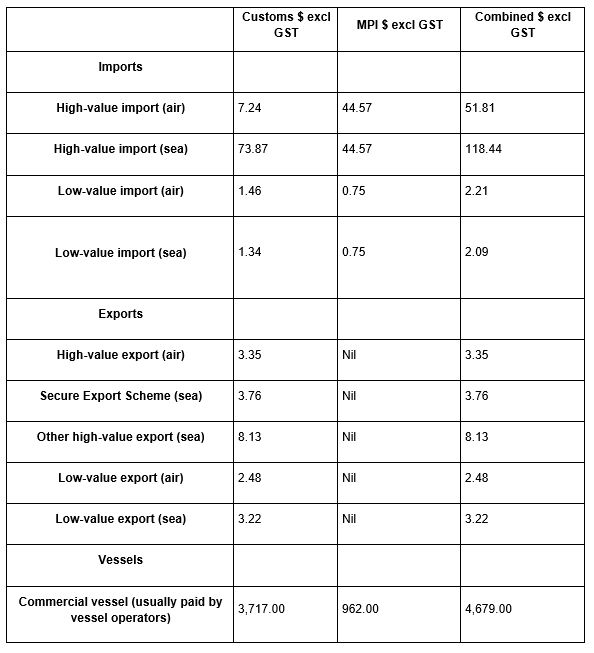

- From the 1st of April this year NZ Customs are changing the costs for entry processing and other fees. These fees were agreed by cabinet in November last year following consultation that started in March 2025. The new fees split out air and sea shipments and high and low value shipments. These are significant changes in the processing fees. If you have any questions, please contact your Oceanbridge Representative.

Fees and Levy rates to apply from 1 April 2026

Below is a table showing the new structure of fees and levies to apply from 1 April 2026. “High-value” means consignments valued over $1000, and “low-value” means consignments valued at $1000 or less.

Below is a table showing the new structure of fees and levies to apply from 1 April 2026. “High-value” means consignments valued over $1000, and “low-value” means consignments valued at $1000 or less.

Australia

LANDSIDE & CUSTOMS

- As Australia enters peak reefer season, exporters of hay, grain, and other perishables continue to face container shortages across multiple shipping lines. Demand remains particularly high for 20GP, 20RF, 20FQ, and 40RF units, creating ongoing pressure on supply chains for temperature-sensitive and bulk agricultural shipments.

- Fuel shortages are still ongoing due to the Middle East crisis. Reports of petrol stations running out of fuel and limits on petrol purchases (including an embargo on filling up jerry cans etc) persist, and fuel surcharges continue to increase for domestic and interstate transport. Please speak with your customer services rep for the latest fuel surcharges as they continue to change on a daily basis.

- There has been a significant increase in Air and Sea shipments on Border Hold as well as increasing delays for shipments held on Border Hold (ABF Border, Redline and Examination holds). Increased shipment volumes, system outages and more complex examinations required have exacerbated the issue, with some shipments being held up to one month. Australian Border Force will not provide estimated release time frames while cargo is on hold, nor will they give reasoning as to why cargo is held. Please be aware that cargo will still incur detention and demurrage while at the port whilst on Border Hold. The ABF has put on extra staff to work through the backlog. Please allow for additional time buffers when planning shipments, and manage downstream expectations as much as possible. While these delays are out of our control, our Customer Service and Landside teams will continue to monitor and provide updates for those shipments impacted.

- 20’ and 40’ Reefer shortages persist in localised areas in the USA, please build additional time into your supply chain for containers to be repositioned.

- Due to a recent discovery of wood-boring insect activity on a set of imported coat hangers by a member of the public, DAFF has implored importers, retailers and consumers to remain vigilant and report any suspected pest activity on imported wooden or timber products. The Department recommends reporting the issue through the national biosecurity hotline 1800 798 636 or via the online reporting system.

- The East-West rail line recovery works are still going. The Melbourne to Perth rail corridor has returned to service, however the Sydney to Perth rail line still remains closed, with re-opening not expected before the 27th March.

- In the Northern Territory, severe flooding across the Kimberley region has closed several key freight routes. No reopening timeframe has been advised. All services to and from Darwin remain suspended due to flooding in the Katherine region, with local depots closed for staff safety and reopening only once conditions allow. Pick-ups and deliveries within the Katherine area are postponed, with many roads not expected to reopen until early next week, subject to weather conditions.

- In Southeast Queensland, severe weather and flooding are affecting transport routes, with delays expected across Gympie, Kingaroy, the Sunshine Coast, Caboolture, and the Rockhampton and Emerald regions. Please anticipate delays of up to three business days, subject to weather conditions.

Asia

AIR

IMPORT

- Transit times and rates are now starting to increase for New Zealand imports, with fuel surcharges likely from 1st April.

- Capacity and rates from the remainder of Asia remain steady for New Zealand imports, but likely to change in the coming weeks.

- Australian import market has stabilised post-Chinese New Year, however the ongoing Middle East conflict is now a key driver across all lanes.

- Reduced overflight options and re-routing of aircraft are impacting schedules and overall global capacity.

- Capacity remains tight across SYD, MEL, and BNE as airlines adjust networks.

- Rates for Australian imports remain elevated, with additional fuel surcharge increases implemented across multiple carriers.

- Delays of 1–3 days for Australian imports continue across key Asian gateways due to network congestion and flow-on disruption from global re-routing.

- South China operations have improved, though not yet fully back to pre-CNY efficiency.

EXPORT

- Consols moving as booked with capacity available on most carriers, rates remain steady but fuel surcharges coming on the 1st of April.

- Capacity remains tight for Australian exports, further impacted by aircraft and network displacement caused by the Middle East conflict.

- Airlines continue prioritising higher-yield cargo, limiting general freight uplift.

- Rates remain elevated, with fuel surcharge increases across most carriers.

- Some uplift delays being experienced due to constrained space and schedule adjustments for Australian exports.

- Early bookings strongly recommended.

OCEAN

IMPORT

- We continue to see constant changes to Emergency Fuel/Bunker Surcharges and we are sending separate notices out for these.

- Space remains mostly open with a few challenges depending on origin and shipping line.

- There are shortages of reefer containers from some Northern China ports, resulting in shipping lines are prioritising Operating Reefer bookings rather than NORs.

EXPORT

- Some Carriers are still experiencing transhipment delays in Singapore.

- As we enter peak season space has tightened, please place your bookings a minimum of 4 weeks in advance of the desired shipment date. Reefer space and equipment is in high demand.

Trans-Tasman

AIR

IMPORT

- Blocked space consols for New Zealand are having some uplift issues, additional space is harder to get particularly due to the lack of freighters coming through Australia.

- Rates remain steady but fuel surcharges starting on the 1st April.

- Major terminals (Qantas Freight, Dnata, Swissport, Menzies) remain operational.

- Slight increase in dwell times due to higher volumes and irregular arrival patterns.

EXPORT

- Consols moving as booked with surprisingly capacity available on most carriers, maindeck shipments are still taking longer to get away.

- Terminals operating normally across all major gateways.

- Increasing forward bookings and tighter space expected for Australian exports as global disruption continues.

OCEAN

IMPORT

- Transtasman services remain relatively stable with occasional omissions or schedule adjustments. At the time of writing this, no significant backlog or congestion to contend with. Cover bookings on transtasman services can still be made 5-6 weeks in advance signalling space remains available in the foreseeable future.

- 20’ equipment remains tight across all ports with primary industries still in export season full swing. Converting consignments from 20’ containers to 40’ or 40’HC equipment (larger orders or less frequent shipments) improves the odds of availability as per your requirements. If more frequent but smaller orders were required, please consider our weekly LCL services to New Zealand.

- We have ongoing rail closures on the South Australia rail network due to Flooding. This is part of the Trans-Australian Railway linking Perth with Adelaide and the eastern states and is a key freight corridor.

EXPORT

- All NZ export services have immediate availability.

Europe

AIR

IMPORT

- Capacity remains stretched particularly for maindeck shipments, our consols via Asia are starting to get delayed in transit and all ad-hoc bookings are experiencing heavy delays.

- Rates have increased across all origins and fuel surcharges to increase from the 1st of April.

- Emirates Airlines are back to a semi-regular schedule however cargo is largely uninsured, Qatar are still embargoed until at least the 28th of March however they are flying some of their freighters.

- Significant impact from the Middle East conflict, with longer routings and reduced available capacity into Australia.

- Emirates (EK) services ex Europe are progressively returning, helping ease pressure slightly.

- Qatar Airways (QR) uplift remains constrained, with no major recovery in capacity at this stage.

- Rates remain elevated, driven by both demand and increased operating costs (fuel and longer flight times).

- Moderate delays continue across European origins, compounded by network disruptions.

EXPORT

- Very limited capacity via Middle East and Asia. Asian freight rates to Europe are almost 3 times higher than from New Zealand so take priority. Space via the USA now very tight as seasonal US carriers start to cease services next week, bookings taking up to 7 days to get secured.

- Outbound capacity for Australia impacted by reduced network efficiency and longer routings via alternative corridors.

- EK reintroduction is providing some relief, though overall capacity remains below normal levels.

- QR capacity still limited, with no significant improvement yet.

- Fuel surcharge increases continue to push overall rate levels higher for Australian exports.

- Moderate delays remain possible depending on routing.

OCEAN

IMPORT

- Most services are open for bookings, however some lines may introduce Emergency Fuel Surcharges due to rapidly rising oil prices.

- BMSB season has started again on September 1st 2025 and will run to April 30th 2026. Procedures are mostly the same as last season. Some sailings from Europe are now due to arrive after April 30th so no BMSB processes needed on these.

- CMA CGM and Maersk are continuing to sail via Cape of Good Hope. There is potential for congestion to build up in Asia at the transshipment ports.

- MSC has some Panama options available.

- We have seen increased customs inspections from European ports particularly on cargo with any military connection.

EXPORT

- All services to the Gulf States have been suspended due to the conflict in Iran. Some Carriers are operating services to Aqaba, Jeddah and King Abdullah from the Mediterranean Sea.

- European ports are experiencing persistent congestion across major container terminals due to a combination of structural, operational, and external disruptions. European port congestion is heavily exacerbated by labour dynamics—shortages, wage negotiations, and strike actions—interacting with automation, winter weather, and infrastructural limitations. Workforce issues remain both a primary driver of operational delays and a focal point for technological and managerial strategies aimed at restoring efficiency in European shipping networks. High demand for port services is outpacing existing capacity (especially in Rotterdam, Hamburg, Antwerp).

- Suez Canal Situation – The Suez Canal attacks continue to cause container lines to avoid the route. Services continue to sail around the Cape of Good Hope.

North America

AIR

IMPORT

- Rates for New Zealand consol cargo still remains steady. So far tariff’s have remained steady with no increases yet. However, we are waiting for the April tariffs to be published which will likely increase and include fuel surcharges.

- New Zealand consols are starting to get delayed in transit, at this stage just by 24 to 48 hours however this is likely to increase.

- Market remains relatively stable for Australian imports, though indirectly impacted by global network shifts.

- LAX congestion persists, with transit delays of 1–3 days on consolidations.

- Fuel surcharge increases continue to push overall rate levels higher for Australia.

- Airlines are actively managing payloads due to longer routings and operational constraints.

EXPORT

- Capacity is full for New Zealand exports due to all the additional European cargo transiting USA. We can get space quicker to the West Coast than the East but still require around 7 days for bookings to be confirmed, this is likely to be extended due to seasonal US carriers ceasing services next week.

- Some minor delays continue due to operational constraints and weather for Australian exports.

- Uplift availability remains generally good for Australian exports, though flow-on effects from global network disruption are evident.

- Fuel surcharge increases continue to push overall rate levels higher for Australia.

OCEAN

- Vancouver – terminal utilization has reduced to 71%, there are no berthing delays. The average import rail dwell time has reduced to 1.9.

- Panama Canal services for ANP/OC1 service – Space is readily accessible, we do encourage that bookings are placed in 2+ weeks in advance of departure.

- US Terminal Operations:

New York – berthing delays of up to 5 days. Import rail dwell time has reduced to 0.3 days.

Norfolk – berthing delays of 15 hours, import dwell time has reduced to 1.9 days.

Charleston – berthing delays of 9 hours, import dwell has reduced to 3.7 days.

Savannah – average wait time for a berth remains at 2 days, import dwell time has increased to 6.2 days, rail dwell time has increased slightly to 1 day.

Houston – no waiting time for a berth. Import dwell time has decreased to3.9 days. Barbours Cut Container Terminal has 4 new STS cranes in commissioning status. The operational date is May 2026.

Oakland – no berthing delays. Average import delivery timeframe decreased to 4.8 days.

Seattle – no berthing delays. Rail import dwell time remains at 3 days.

Long Beach – congestion on port is 5.4 days.

IMPORT

- There are significant increases to fuel costs for all inland rail and trucking moves with a lot of those changes subject to change with limited/no notice.

- Space on vessels is unencumbered at this time.

EXPORT

- US Tariffs – current status:

- Court Orders and Timeline

- On March 4, 2026, the CIT issued a sweeping refund directive in Atmus Filtration, Inc. v. United States.

- The Court instructed U.S. Customs and Border Protection (CBP) to refund tariffs for:

– Entries not yet liquidated (to be retroactively cleared)

– Entries within the 180-day protest window (to be reopened for refund) - Immediate compliance was suspended after CBP indicated logistical impossibility.

- CBP Response and CAPE Portal

- CBP proposed a Consolidated Administration and Processing of Entries (CAPE) portal, aimed at automating refund processing.

- CAPE functionalities:

- Uploading standardized lists (CSV) of entries.

- Automatic recalculation of duties without IEEPA tariffs.

- Reviewing and setting liquidation/refund dates.

- Electronic payments to importers’ bank accounts.

- As of March 12, 2026, development was 40–80% complete, with a target rollout around Mid-April 2026

(approximately 45 days from early March).

If your business is the Importer of Record with CBP and need to apply for duty refunds, please contact your Oceanbridge representative for guidance.

- Court Orders and Timeline

- West Coast North America – the direct service to West Coast of the US & Canadian is seeing a drop off in demand, the Vancouver calling vessels remain at capacity. There is a blank sailing in Week 16, effectively there is a 3-week gap between Vancouver and Seattle departures in April. Effective the Seaspan Hamburg 617N, ETD Tauranga 14/5, vessels will call at Long Beach Fenix Marine Services terminal and no longer discharge at Long Beach.

- US Customs holds/inspections – Containers selected by US Customs for examination are taking 1-3 weeks to be inspected; Long Beach is the most impacted port with delays.